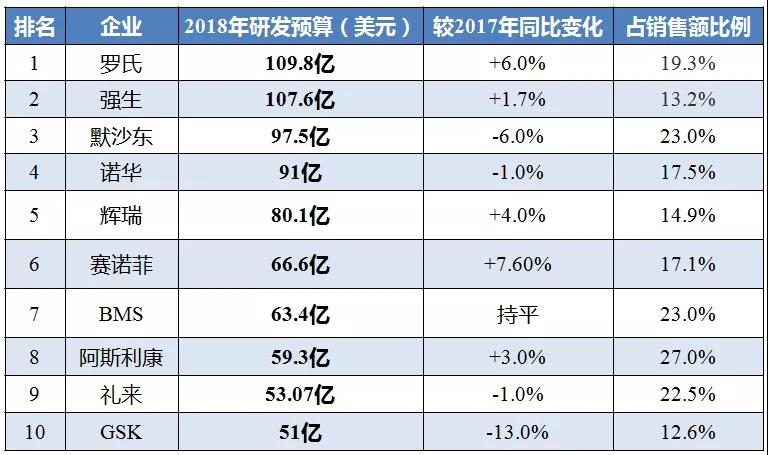

On June 5, as many as 38 (64%) of the 59 new drugs approved by the US FDA last year were originally from emerging biopharmaceutical companies. In drug development, small biotech companies have become more important than their mass. However, the traditional giants in terms of capital investment are still "rich and rich." FierceBiotech pointed out that last year, the total amount of global sales of Top 15 pharmaceutical companies in research and development exceeded 100 billion US dollars.

In terms of R&D spending, Roche, Johnson & Johnson (J&J), Novartis, etc. are still unattainable. Last year, Roche once again topped the list with $11 billion (including diagnostics).

In fact, the rankings and amounts of pharmaceutical giants' R&D spending have not changed much in recent years. Roche has been in the first place for several consecutive years, despite a reduction of nearly $500 million in research and development spending compared to 2016. At the same time, Sanofi has increased its number of M&A transactions from $5.45 billion in 2016 to $6.6 billion in 2018; Merck, which has more than 1,000 clinical trials for star product Keytruda, Although it fell from $10.33 billion in 2017 to $9.75 billion in 2018, it is still much higher than the $7.19 billion in 2016.

Here are the top ten pharmaceutical companies with the most research and development expenditures in 2018:

1 , Roche: Dealing with the "patent cliff" challenge

In order to save money and increase investment in research and development lines, Roche reduced its marketing and sales departments last year, and this trend will continue in the next few years.

Roche is facing the challenges of the expiration of three major products, Rituxan, Herceptin, and Avastin. Last year, these three drugs totaled Roche's contribution. 36% of the income. At present, its "new star" product Octrovus is growing rapidly, and there are also heavy varieties such as PD-L1 product Tecentriq, type A hemophilia treatment Hemlibra and influenza medicine Xofluza.

In addition, there are 16 new drugs in the Roche post-development line. Two of them will be reviewed this year for polatuzumab for lymphoma and entrectinib for treatment of NTRK fusion-positive solid tumors.

Roche's R&D budget is not all invested in new drugs, but also in the improvement of old drugs. For example, the study of implantable devices for Lucentis extends the administration time to half a year or even a year; there is also the effect of trastuzumab and pertuzumab (trastuzumab). Combined drug test.

The related actions of pharmaceutical mergers and acquisitions also highlight Roche's ambitions in research and development. Last year, a partnership with 4D Molecular Technologies led to the first step in the layout of gene therapy, and this year's acquisition of Spark Therapeutics further strengthened Roche's presence in the field.

Of course, Roche's research and development line will inevitably have several projects "abortion", the most concerned about which is the discontinuation of the new AD drug crenezumab.

2 , Johnson: M & A frequently "step on the thunder"

Like Roche, Johnson & Johnson's R&D budget also includes non-pharmaceutical business. For Johnson & Johnson, it seems that there have been some “unfavourable years†in the past year, and several projects that have been acquired through trading have suffered setbacks. In October last year, Johnson & Johnson announced the termination of a clinical trial of a drug for infant respiratory syncytial virus (RSV) treatment. The drug was acquired by Alios in 2014; a month later, Johnson & Johnson gave up the rheumatoid arthritis drug FR104, which was introduced in 2016 with a prepayment of $11 million.

Johnson & Johnson continues to bet. Last year, it acquired the global rights of Arrowhead's hepatitis B RNAi drug for $175 million. In October, Johnson & Johnson's Janssen paid $300 million in advance payments to develop treatments including Aroeia with Argenx. CD70 antibody cusatuzumab of various cancers. At the same time, Janssen and his collaborators reported the positive results of a 1/2 clinical trial of their CAR-T therapy.

This year, Johnson & Johnson's Spravato was approved for marketing, the first anti-depressant with a new mechanism of action in 30 years.

3 , Merck: Keytruda trials over a thousand

To build more than 1,000 trials for the "blockbuster" Keytruda, it's no wonder that Merck's R&D budget has increased a lot in the past few years. Combination therapy research is hot, and many pharmaceutical companies are arranging and combining Keytruda. This is good for Merck, but some analysts caution that excessive reliance on a product should be avoided in case it becomes a case of Aumivum (Humira). This year's acquisition of Immune Design is an attempt by Merck to strengthen its R&D line.

Last year, Merck's high-profile anti-cancer drugs were hit hard, and at the ESMO meeting, the invalid data of STING agonist MK-1454 monotherapy for advanced solid tumors and lymphomas were published. STING agonists are the research and development hotspots in the field of anti-tumor. Johnson & Johnson and Novartis have their layouts, and the data released by Merck also poured a cold water on the field.

In addition to Keytruda, Merck is also a key investment in the vaccine business. Currently, there are 4 products in the late research and development line, including Ebola virus vaccine, varicella-zoster virus vaccine, pneumococcal vaccine, etc., the latter will be directly related to Pfizer ( Pfizer)'s Prevnar competes in the market.

4 , Novartis: Welcome to the new drug harvest year

With Vas Narasimhan in charge, Novartis made a major overhaul of its R&D business last year. About 90 projects were cut (up to 20%), focusing on cutting-edge new drug development efforts.

This year will be a bumper year for Novartis, and four drugs will be reviewed. Among them, the well-received SMA gene therapy Zolgensma and the PI3K inhibitor alpelisib for breast cancer have been approved recently. Mayzent, a multiple sclerosis drug, was also approved in March this year.

In a series of projects last year, “Slimmingâ€, Novartis sold the infectious disease business to Boston Pharma, and sold the shares of consumer health companies that are joint ventures with GlaxoSmithKline. In addition, Novartis sold the oral solids business to Aurobindo and split the eye care business unit Alcon, rumored that its generics business unit Sandoz may also be split. .

At present, Novartis has taken the lead in the field of cell therapy, holding the CAR-T product Kymriah. Last year, the acquisition of AveXis for $8.7 billion further consolidated its position in the field of gene therapy. Currently, Novartis's gene drug research and development lines cover areas such as eye diseases, nervous system diseases, and hearing loss.

5 , Pfizer: Strive to launch 15 "blockbusters"

Pfizer’s R&D spending increased 4% year-on-year last year, mainly to some mature pipelines, such as the Phase III clinical trial of the JAK1 inhibitor abrocitinib for dermatitis, and the development of the C. difficile vaccine – due to Sanofi’s development in 2017. Failed to exit, making Pfizer in the lead. In addition, Bavencio, a tumor immunopharmaceutical developed by Pfizer in cooperation with Merck KGaA, has entered the final sprint phase and is costly. The drug has been approved for the treatment of bladder cancer and Merkel cell carcinoma, followed by competition with companies such as BMS and Merck.

On the other hand, due to the failure of clinical trials, Pfizer terminated its two studies on the drug dumagrozumab for Duchenne muscular dystrophy, abandoned the third-generation EGFR inhibitor mavelertinib for non-small cell lung cancer research, and abandoned the anti-IL7R antibody. The study of type 1 diabetes has also abandoned the study of a subset of CAR-T lines and CD137 agonist antibodies.

This year, Pfizer has a total of 100 research projects, including 26 in Phase III, 28 in Phase II, and 11 in Pre-registration. If Pfizer wants to achieve the goal of launching 15 “blockbusters†during 2015-2022, it will need to maintain the vitality of these R&D lines.

Under pressure, Pfizer made a major restructuring last year – all innovative drug divisions under the Pfizer Biopharmaceutical Group, separate from the Consumer Health Products division, with the goal of streamlining management processes and freeing up R&D and business development. cash.

6. Sanofi: Strengthening internal research and development capabilities

Among the top 10 companies on the list, Sanofi's R&D investment increased the most. Last year, due to changes in leadership personnel, Sanofi adjusted its research and development line – terminating 13 clinical phase projects and 25 preclinical research projects, with a focus on tumor immunity, rare diseases and rare blood diseases.

A batch of new drugs entered Phase III clinical trials last year, including the hemophilia drug fitusiran, the multiple myeloma drug isatuximab, for the rare blood disease, the drug for cold agglutinin disease, Bioverativ, etc.... With these pipelines concentrated into delivery During the period, Sanofi’s total R&D expenditure increased significantly.

On the other hand, the company was succumbed to the development of diabetes drugs, and its dual GLP-1/glucagon receptor agonist drug tolerance for metaphase diabetes was terminated in November last year. Two cancer antibody-conjugated drugs (ADCs) have failed to progress as expected—one of the CA6-targeted drugs suffered a failure in a phase II clinical trial of triple-negative breast cancer, and anti-LAMP-1 antibody drugs against solid tumors It has also been discontinued in clinical trials for the treatment of multiple sclerosis.

Recently, Sanofi is trying to reduce its dependence on external partners in research and development and strengthen its basic research capabilities. About 50% of the compounds currently under research are from the company's internal research and development channels, and Sanofi hopes to increase this number to 70% in the next 5 to 10 years.

7 , BMS : Super M&A to be inspected

Bristol-Myers Squibb (BMS) investment in research and development last year and the year before last on the flat, and for just a $ 74 billion acquisition of the new base Medicine (Celgene) - BMS implementation of the pharmaceutical industry's largest turnover of a merger, the question of The sound is endless - many people doubt whether Opdivo (O medicine) can reach the expected sales scale.

This is because the company's O drug combination data released at the ASCO meeting last year is not enough to make BMS invincible, and the bladder cancer pipeline data released in February this year failed to attract enough attention.

Like competitor Merck, BMS has focused most of its efforts on oncology-targeted drugs or immuno-drugs in recent years – the introduction of Yervoy and O-drugs. However, unlike Merck, O medicine has not reached the height of K medicine in terms of clinical data and sales. For BMS, it is time to step up the pace of advancing its clinical pipeline and experimenting with more cocktails. Some commentators pointed out that it will take time to prove whether the acquisition of Xinji Medicine can really promote the clinical progress of O medicine.

BMS currently has 38 compounds under development, and the research and development line covers a variety of areas, including cancer, cardiovascular disease and fatty liver diseases.

8 , AstraZeneca: performance returns to growth

For AstraZeneca, 2018 was a year of transition for all aspects of business and began to resume sales growth. In recent years, AZ has marketed a number of new anti-cancer drugs, including EGFR inhibitor Tagrisso (osimertinib) for non-small cell lung cancer, PARP inhibitor Lynparza (olaparib) for ovarian and breast cancer, and tumor immunopharmaceutical Imfinzi (durvalumab). ).

By the end of 2018, AZ had 22 projects in the late stage of development. For the new drug, the only drug candidate is PT010, a single-inhalation, fixed-dose triple therapy, budesonide [inhaled corticosteroid (ICS)] and glycopyrrolate [a long-acting effect] Muscarinic agonist (LAMA)] and formoterol fumarate [a long-acting beta 2 agonist (LABA)].

Among the AZ intermediate drug candidates, the new AKT inhibitor capivasertib for triple-negative breast cancer and prostate cancer, the PT027 (Budesonide/salbutamol) for asthma on demand, and the potential first-in-class TSLP inhibitor for severe asthma Tezepelumab is the most outstanding performer.

However, in 2018, the list of projects abandoned by AZ was quite extensive. The results of the MYSTIC trial of Imfinzi (Durvalumab) in combination with the CTLA4 inhibitor tremelimumab in the treatment of stage IV non-small cell lung cancer did not reach the end point of improving overall survival (OS). In addition, it discontinued a global Phase 3 clinical trial of Lanabecestat, an oral beta-secretase lyase (BACE) inhibitor for Alzheimer's disease, in collaboration with Eli Lilly.

9 , Lilly: AD drug development frustrated

For Lilly, 2018 is mixed. In June, it abandoned the Phase 3 trial of the BACE inhibitor lanabecestat in combination with AZ for Alzheimer's disease, and in November abandoned another study of early BACE inhibitors.

It is worth noting that anti-cancer drugs are still the focus of Lilly's research and development pipeline. Last May, Lilly invested $1.6 billion in Armo Biosciences and its main asset, pegilodecakin, which has shown promise for single-agent and combination therapy for multiple oncological diseases.

In the first week of 2019, Lilly announced the acquisition of Loxo Oncology for $8 billion. Through this acquisition, Lilly will receive Loxo's targeted drugs for cancer, including half of the already marketed pan-tissue anticancer drug NTRK inhibitor Vitrakvi, another pan-tissue drug RET inhibitor LOXO-292, one in one The BTK inhibitor LOXO-305 and several preclinical products.

10 , GSK : return to the field of anti-tumor

GlaxoSmithKline's (GSK) strengths are concentrated in the three major areas of respiratory disease, AIDS and vaccines. As early as 2014, GSK made major business adjustments, replacing the entire anti-tumor business assets with Novartis's vaccine business assets (excluding Novartis's flu vaccine). With the rise of tumor immunotherapy, GSK has renewed its anti-tumor business as one of its strategic priorities and has cut some of its early research and development projects to improve R&D efficiency.

At the same time, GSK continues to work externally on anti-tumor business. The data show that there are currently two Phase II projects in the GSK tumor pipeline, including TCR-T cell therapy, antibody-conjugated drugs targeting BCMA, and six Phase I projects, including targets such as BET, OX40, TLR4, and PI3K.

In December 2018, GSK announced the acquisition of Tesaro for $5.1 billion. The latter product, Zejula (Niraparib), is an oral poly ADP ribose polymerase (PARP) inhibitor that is currently approved for ovarian cancer in the United States and Europe. In addition to Zejula, TESARO also has anti-tumor drugs including PD-1 and Tim-3. However, there are also Wall Street analysts who believe that Tesaro's drug pipeline lacks an intersection with GSK and it is difficult to produce synergies.

Clearly, GSK's determination to enter the anti-tumor business is very determined. In February of this year, GSK and Merck announced that they have reached a global strategic cooperation alliance to jointly develop a dual-function fusion protein tumor immunotherapy M7824 (bintrafusp alfa) targeting PD-L1/TGF-β, with a total transaction volume of 3.7 billion euros.

Virus Sampling Tube,Virus Sampling Kit,Disposable Vtm Sampling Kit,Vtm Sampling Tube With Swab